Did you have to read the headline twice to make sure you weren’t seeing things? Because amidst recent property market news you surely know that house prices are at an all-time high and that the monthly numbers, frankly, are becoming almost comedic in their relentless climb. This week’s Rightmove asking price data certainly attests to that. Again.

The latest index from the Halifax points to chunky month on month house price rises too, a 1.4% boost in April compared to March – a record high for two months on the trot.

The Nationwide Building Society and the Office of National Statistics are similarly bursting with outsize stats and which are all reaching for double digit annual increases in property values.

But, and here’s the thing, UK house prices are actually incredibly affordable and even more so than ten years ago.

‘Seriously?’, you ask. ‘You must be deluded’. Well, no, because despite the hyperbole around the market right now the official data supports my initially fantastical contention that you are better off buying a home than you were at any time since Maroon 5 encouraged us to Move Like Jagger.

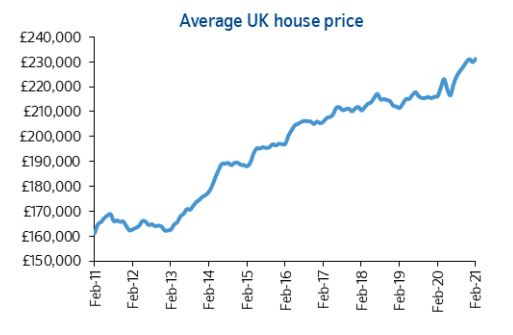

You see, house prices may have shot up from £173,800 back then to £268,300 now, a hike of 54%, but there are other factors at play that mitigate this seemingly unaffordable escalation.

First, most properties are purchased with a mortgage and mortgage rates are 56% lower than they were in 2011 – typically 1.62% for a 2-year fixed rate deal versus 3.7%. This means that actual affordability for the majority of folk is now in line with a decade ago when you accept that ‘affordability’ is exactly that – what you can afford to pay.

Second, when you adjust the average house price for inflation, the 2011 value is far less of a stretch at £216,600.

Third, the absence of stamp duty on all purchases up to £500,000 in recent months removes another layer of buyer friction.

Factoring for inflation plus mortgage rates plus the Exchequer’s take too, makes for a somewhat more positive and honest narrative altogether and now, I’d argue, one can see why house prices are so easily prone to increase at what are thought to be such eye-watering rates – simply because they are actually much more affordable than we all perhaps give credit for.

Factoring for inflation plus mortgage rates plus the Exchequer’s take too, makes for a somewhat more positive and honest narrative altogether and now, I’d argue, one can see why house prices are so easily prone to increase at what are thought to be such eye-watering rates – simply because they are actually much more affordable than we all perhaps give credit for.

And so, I’m sincerely sorry to all today’s would-be first time buyers clambering for that elusive foot on the first ladder rung, but it looks like onwards and upwards still further I’m afraid.

And as for estate agents, your stall is firmly laid out as one where hot-cakes remain the order of the day for a while and probably even after the stamp duty festivities end next month.

But there’s a but. The concern is not whether demand will naturally subside this year and if Sunak’s gradual unwinding of subsidies will dilute transactions to a normal level again, depriving you of the best months you’ve ever had. No, it’s the spectre of inflation rising sharply in the coming months as consumer spending, raw material costs, fuel and house prices overheat an economy in celebratory mood. Because those of us with a few years in the game remember what happens to this industry when there’s a boom and it’s nearly always followed by bust as interest rates are hiked by our Central Bank to kerb the ‘danger’. That, after all, is their core function.

Consequently, the property market rollercoaster will remain well-travelled and its recent dizzy heights may inevitably lead to a downward corkscrew around the next corner.

I’m a market optimist by nature and as those betting types that wrongly disagreed with my positivity over 2020 house prices now know to their cost. But the coming combination of consumer demand unleashed, abundant cheap money and the aforementioned, relative affordability of housing, are all exactly what led to us hitting the buffers in the late 1980’s and, to an extent, in 2008 too.

I’m a market optimist by nature and as those betting types that wrongly disagreed with my positivity over 2020 house prices now know to their cost. But the coming combination of consumer demand unleashed, abundant cheap money and the aforementioned, relative affordability of housing, are all exactly what led to us hitting the buffers in the late 1980’s and, to an extent, in 2008 too.

So, enjoy the ‘post-pandemic’ ride for a while. But with much caution and your wits about you.

Comments (12)

Unfortunately the Quirk does talk some sense here. This and previous governments have introduced regular help to buy schemes which do nothing more than stoke up demand and as my O’ level teacher would say, in an inelastic supply market, this only leads to higher prices, (making it harder for first time buyers!) As said in another article today, prices have been rising the fastest since just before the last crash. That has to tell people something surely.

I hear you, but structurally things are the polar opposite of 08, that was a liquidity crisis, this is the government spending ££££ carpet bombing the economy, there is no precedent in my life time.

Whenever people say ‘It’s different this time’. That is the time to sell, sell, sell!

Which is what we’re doing goddamnit!!!!!!

[Sentence removed as it breached posting rules] He doesn’t seem to appreciate that the banking system and property market is at risk of collapse due to the millions of worthless flats. Leaseholders aren’t in any position to pay the full remediation costs which makes the flats worthless. Millions of leaseholders will be bankrupted and lenders won’t receive a penny as Freeholders will repossess. They will then have to pay the full remediation costs. Then they can sell the flat again for full market price. The housing market will continue to boom due to scarcity as nobody with any sense will buy a flat. It is reckoned that it would cost about £50 billion to remediate properly all the defective flat blocks in the UK. I would suggest that is a very cheap price to save the UK property market. Govt could pay all the remediation costs and then recover from those responsible. Invariably it is just not worth leaseholders paying remediation costs. Most could be discharged bankrupts in a year. That prevents lenders pursuing recovery of defaulted mortgages which would last 12 years unlike the 6 years for other defaulted credit. Yes it means the bankruptcy will be on credit files for 6 years. Big deal!! At least the leaseholder will have evaded an impossible situation which they should never have been liable for in the first place. Leaseholders are being forced to carry the can for incompetent construction firms and Councils for over 45 years. Leaseholders should just give up. If Quirk thinks none of this will affect the UK property market he is deluding himself. No way would I even consider buying a flat. That is why the house market is going mental. Normally flats would be bought but no buyers are interested in flats. Apparently these EWS1 forms are only valid for 5 years. Then what!? Supposing a new inspection reveals other faults!? You’d have to be out of tiny mind to buy a flat. Houses are the only game in town which is why the house market is appreciating in value so much. With millions of dud flats houses will continue to be in great demand which accounts for the stupendous increases in house prices. The other advantage of a house is that invariably value may be added to it. Can’t do that with a worthless flat! Many leaseholders have yet to face up to the reality of their circumstances. Bankruptcy is the only really viable course of action available to them. They should start liquidating what other assets they have into cash which can be hidden away. Then file for personal bankruptcy. There are unfortunately many leaseholders who will lose their livelihoods as bankruptcy terminates their jobs. These particular leaseholders are in an impossible position. They can’t go bankrupt but can’t afford the remediation costs! But they will be made bankrupt whether they like it or not. The state of the flat market is a massive Sword of Damocles hanging over the UK property market. The Credit Crunch will be a minor detail compared to millions of worthless flats. Banks will need to make massive provisions for losses that will be occurring. We are talking billions here. Are banks resilient enough to weather millions of worthless flats! If I had any savings with banks I’d certainly pull them ALL out………………..just in case!! Remember Northern Rock!! Govt hasn’t understood the true ramifications of failing to deal with the flat remediation problems. They will find out very shortly that their incompetent and inadequate response to the plight of innocent leaseholders will come back to bite them in the most severe of ways. A degrading of the UK property market.

Oh dear. Honest the sun will shine one day for you

I think somebody bought a flat with a dodgy lease.

Would that be the flat he tried to tell us he was selling for FREE? That it was the future and regular High Street Agents were toast in the grilling?

That apparently didn’t pan out well.

Anyone got any magic beans they want to offload? This guy is your buyer!

“The shock truth is the UK housing is most affordable in years”

You have to love soundbites. Let me correct this for you; “Depending on where you choose to purchase, the UK housing market is the most affordable in years”.

Very interesting article. I have to agree with you Russell. At the same time I really do feel sorry for first time buyers….even once they manage to pull together a deposit (often with serious difficulty as Mrlondon52 correctly says above) they also still need to deal with the ever increasing prices and a minefield of “helpful” schemes to get on the ladder.

Russell it’s the deposit which is the problem, not the repayments.

58% of tenants have no savings according to Govt data.

No savings – think about it.

(Oh, plus millions of flawed credit histories are a serious problem too)

Predicting continual boom,

I’m sincerely sorry to all today’s would-be first time buyers clambering for that elusive foot on the first ladder rung, but it looks like onwards and upwards still further I’m afraid.

and warning of overheating causing a ‘pop’ in the same article? ———

You’re far from the only person to have predicted the boom. This is overheating rapidly however and broadly the public know it.

FoMo and mania are rife. By November / in November this year the wind blowing through will be a much lower temperature. Only a fool would look ahead much further than Spring ’22.

Given however that logic suggests rate rises against inflation, Vs the fact that global interest rates have been falling for 700 years……

The short term versus the medium and long term are very different animals. Six months is about to prove itself a very long time in the UK housing market.